By

By How to Make the Down Payment for Your New Home with EPF Funds

Getting your first home loan is a pivotal step towards homeownership, but the initial down payment can be difficult. Fortunately, the government has alleviated the burden by allowing withdrawals from the Employees Provident Fund (EPF) as down payment assistance for first-time home buyers.

Before considering EPF withdrawal, you should have clarity on the withdrawal limits, pros and cons, eligibility criteria, and the application process. Let’s take a closer look.

How do EPF withdrawals work?

The EPF fund is divided into Account 1 and Account 2. Every monthly contribution is divided between these two accounts, with 70% going into Account 1 and the balance 30% into Account 2.

The funds in Account 1 can only be withdrawn once you reach the retirement age of 55. Other circumstances include if someone goes on a pension scheme, migrates to another country or becomes disabled.

Account 2, on the other hand, can ease your financial burden in the areas of housing, education, and medical expenses. Thus, one can withdraw from Account 2 to be used as down payment assistance for first-time home buyers. It can also be used for other homeownership expenses such as construction or repayment of monthly housing loans.

How much can I withdraw from EPF for my down payment?

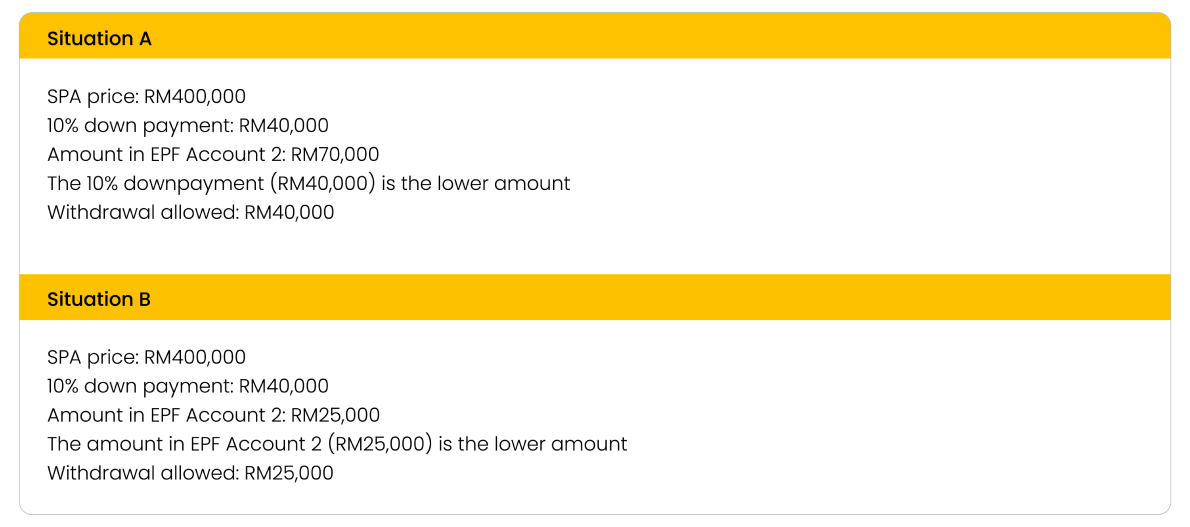

Home buyers typically need to make a down payment of 10% of the Sales and Purchase Agreement (SPA) price, with the remaining 90% covered by a bank loan or self-financing. You can withdraw the full amount needed for the down payment from your EPF Account 2, or all your savings in Account 2, whichever is lower.

Here are some examples.

What are the pros and cons of withdrawing from EPF for my down payment?

Before withdrawing from your EPF Account 2, consider these pros and cons.

|

Pros |

Cons |

|---|---|

|

|

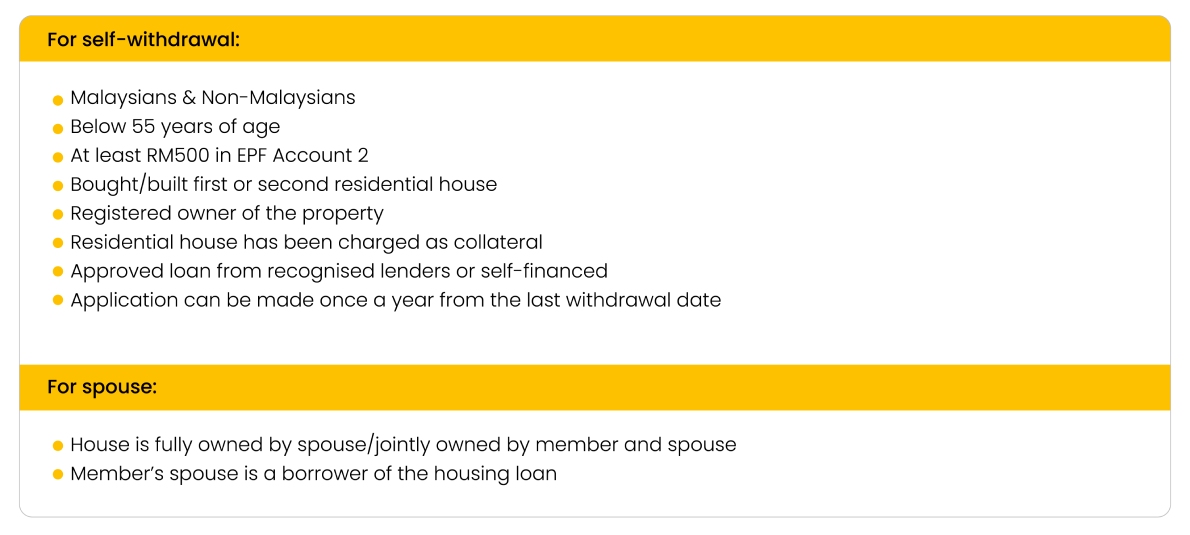

Who can withdraw from EPF Account 2?

To withdraw from EPF Account 2 as down payment you must meet the following criteria:

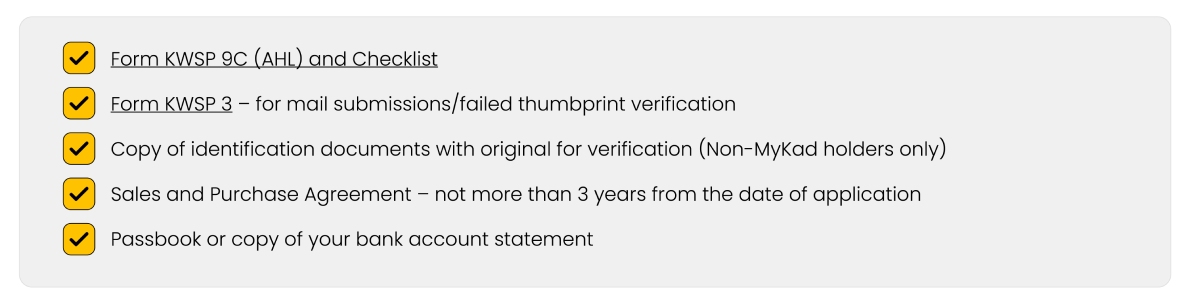

How to apply for withdrawal from EPF Account 2

You can apply via your iAkaun or manual submission according to the instructions on the official EPF website. To apply, you’ll need to have all the following documents:

It’s important to note that you will need to pay for your down payment first before applying for EPF Account 2 withdrawal.

Making the final decision

While withdrawing from EPF Account 2 is an option that can ease the burden for many, not everyone may own the luxury of having sufficient funds in their EPF to cover the down payment. There may also be others who would prefer to leave their EPF untouched for the future.

If this is the case for you, you may want to explore maximising returns on savings to reach your down payment amount earlier. You can do so by using facilities such as ASB and Fixed Deposit, which can grant you higher returns than a standard Current and Savings account.

To find out which properties you can afford before withdrawing from your EPF Account 2, use our home affordability calculator.If you are satisfied with the terms, you can apply online immediately for a hassle-free experience.

💡 The information provided above is purely for educational purposes.

References

1. Employees Provident Fund (EPF). (2023). Withdrawal for House Financing. https://www.kwsp.gov.my/

2. iMoney Malaysia. (2023). Using EPF for Home Purchase: How It Works. https://www.imoney.my/

3. Loanstreet. (2023). A Guide to EPF Withdrawal for Housing Loan. https://www.loanstreet.com.my/

4. PropertyGuru. (2023). How to Use EPF Savings for Your First Home. https://www.propertyguru.com.my/

5. RinggitPlus. (2023). EPF Withdrawal for Housing: What You Need to Know. https://ringgitplus.com/

You may also like

Properties Sale & purchase

28 December 2023

28 December 2023 4 min read

4 min read

Should You Be Buying a Subsale House or a New Property?

Related Products

Maybank Home2u

Hassle-free home financing for just about anyone and everyone.

ASB Financing/-i

Shariah-compliant financing for ASB unit trust up to 35 years or age 70 years old.

eFixed Deposit

A fixed deposit account that gives high fixed rates and lets you manage it all online.

Savings Account-i

A Shariah-compliant savings account fit for the entire family.