You’re thinking about getting into investing. Maybe you’ve heard people talk about how they’ve made a fortune on the stock market, or maybe the thought of making enough money to be able to retire early appeals to you.

While it’s great that you’re ready to take your finances seriously, you should be aware of the common pitfalls that beginners will face when rushing into investing.

Here are five common investing mistakes you should look out for especially if you don’t have much experience around investing.

1. Starting too late

It is never too late to start investing, but there is a huge benefit in having more time. Investing early (called a long investment horizon) gives you one major advantage: compound returns.

Compound returns work by earning returns on top of your investment returns. For example, if you start with an investment of RM1,000 at 5% per annum (or per year), you will have RM1,050 at the end of the first year and RM1,102.50 by the end of the second year.

With this table, you can see how RM1,000 can snowball over a long period of time (assuming average 5% per annum returns).

|

End of Year |

Value (with 5% p.a. rate of return) |

|---|---|

|

1 |

RM1,050.00 |

|

5 |

RM1,276.28 |

|

10 |

RM1,628.89 |

|

20 |

RM2,653.30 |

|

30 |

RM4,321.94 |

As you can see, having more time to invest gives your wealth more time to grow. So, start as early as you can.

However, don't be discouraged if you're already older and don't have an investment portfolio yet. Any amount invested is still valuable to you, so get started as soon as you can. Starting late is better than not starting at all.

2. Not having an emergency fund

Emergencies are unpredictable, and you need to always be prepared for them. In many cases, this means having some extra funds lying around to pay for unforeseen expenses like medical bills or car repairs.

Many new investors have a habit of locking up all their money into their investments in the hope of getting more money in return. In this case, you end up with a situation where you have no liquidity, i.e. no easy access to cash.

This happens because investments are not money, even if they have value. You cannot spend them until you sell your shares and bonds, or get income from dividends. Even then, you need to wait for your trading platform or fund manager to transfer the funds to your bank account (which could take 24 hours or more).

Due to this, you should always keep at least six months’ worth of expenses in an emergency fund. This rule of thumb isn’t a hard rule, and it’s perfectly fine to save a little more just in case. However, you always need savings that are easily accessible in case something happens to you or a loved one.

3. Trying to time the market

Global markets tend to move on a somewhat predictable cycle, and it’s tempting to time the market so that you are able to buy low and sell high - and see big returns in a short amount of time.

This is not as easy as it looks. In most cases, you cannot know if the market really has hit the bottom and is prepared to recover. Or worse, if it will recover the same way. Not every company bounces back, nor does every market. An investment may look like a bargain because the business is on its way to becoming obsolete but if you lack experience as an investor, it may look like an opportunity.

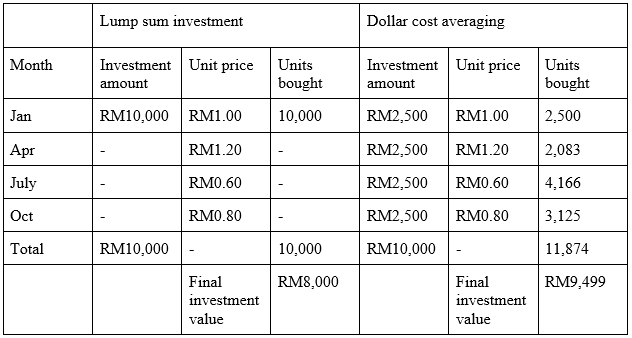

Instead, it is better to invest using the dollar cost averaging (DCA) system. That is, consistently investing in order to spread out losses and gains. This is a good way to increase your chances of winning out in the long run.

This is how it works:

This example shows how the market can rise and fall over time, making it difficult to know when to buy and sell. You could have made a profit if you had sold your investment early, but holding on for longer would have made a loss. The DCA method, on the other hand, would have spread out the risks and reduced your losses from an uncertain economy.

4. Investing based on 'hot tips'

The dream of every investor is to hear about the next big thing before it happens. Everyone wants to invest in the next Apple or Tesla, but that doesn’t always happen.

It’s nearly impossible to predict share prices - even for professionals. There are an infinite number of things that could go wrong. For example, Chinese conglomerate Alibaba’s stock was tipped to rise with an impending IPO of subsidiary Ant Financial. Instead, it dropped by 9.7% after the IPO was suddenly suspended.

This is not to say that analysts will always get it wrong, but rather you should not always be rushing to invest in the next big thing without doing your research first. Particularly if someone is telling you to buy stock in a specific company. Doubly so if your ‘hot tip’ comes from unverified sources shared on social media and chat groups.

5. Investing without doing your homework

Learning to invest takes time. You’re not going to hit it big and become a millionaire overnight. There is a lot of research that goes into understanding what it is you’re investing in, and how you plan on going about it.

For example, you should have already built your investor profile before allocating any funds. How much money can you afford to risk each month? What is your investment horizon? How much risk do you want to take on? What is your goal for all this wealth?

Make informed decisions

Before you begin investing, head over to the Maybank Financial Goal Simulator to start planning your strategy. It helps to get a visual representation of just how much you can afford to invest and how long it will take to reach your financial goals.

If you’ve already begun investing, then why not find out how you’re doing anyway? It’ll help you figure out if you’re on the right track to get to where you need to be or if you need to make some adjustments to your plans.