Do your investment decisions keep you awake at night?

For example, if you have just invested in a stock and the price starts to go down, how far down are you prepared to see it drop before you cut your losses and sell?

Basically, ask yourself how much money you are willing to lose in exchange for the possibility of greater financial return on your investment.

You will need to figure this out so that you will know which types of investments you should look at and which ones you should avoid.

What affects the amount of risk you can take?

Before you start investing, it’s important to know your risk tolerance. Everyone will have a different set of factors that will influence how much risk they should take.

Ask yourself these questions:

What is your investment goal?

Different goals will need a different investment approach to be able to deliver the right return you need. For example, investing to meet your child’s education involves a different strategy to planning for retirement.

How much time do you have?

After setting your sights on a goal, you need to get realistic about the time you have. If you have 20 years to reach that goal, you may be able to take more risk to average out the losses with the potential to make higher profit. However, if you only have five years, you may not have the time to make up for the losses.

What other commitments do you have?

If you are still single and in your 20s, the investing risks you take will probably only affect you but someone in their 40s with three children and existing loan commitments will have to consider how any investing risk they take on will affect all the other areas of their life.

How much risk can you live with?

Even if you have 30 years ahead to manage your investments and you have enough money set aside for emergencies and loan commitments, but the thought of losing money over your investment keeps you awake at night, then you should acknowledge that you are not comfortable with high risk investments.

It’s the combination of all your answers to the questions above that will help you figure out your risk tolerance.

Your risk tolerance will shape your investment decisions

Knowing your attitude towards investment risk will help you understand your own profile as an investor.

Younger investors are usually seen as being able to take on more risk and have a more aggressive risk profile, while those approaching their 40s may start to scale back a little on the riskier investments to a moderate risk profile. Meanwhile, those nearing retirement focus mostly on lower risk options recommended for conservative risk profiles.

However, not everybody falls into these standard classifications of aggressive, moderate, or conservative risk based on their individual risk tolerance.

While it may not be clear what your own risk tolerance is, there’s an easy way to get a personalised risk profile.

Find your risk profile

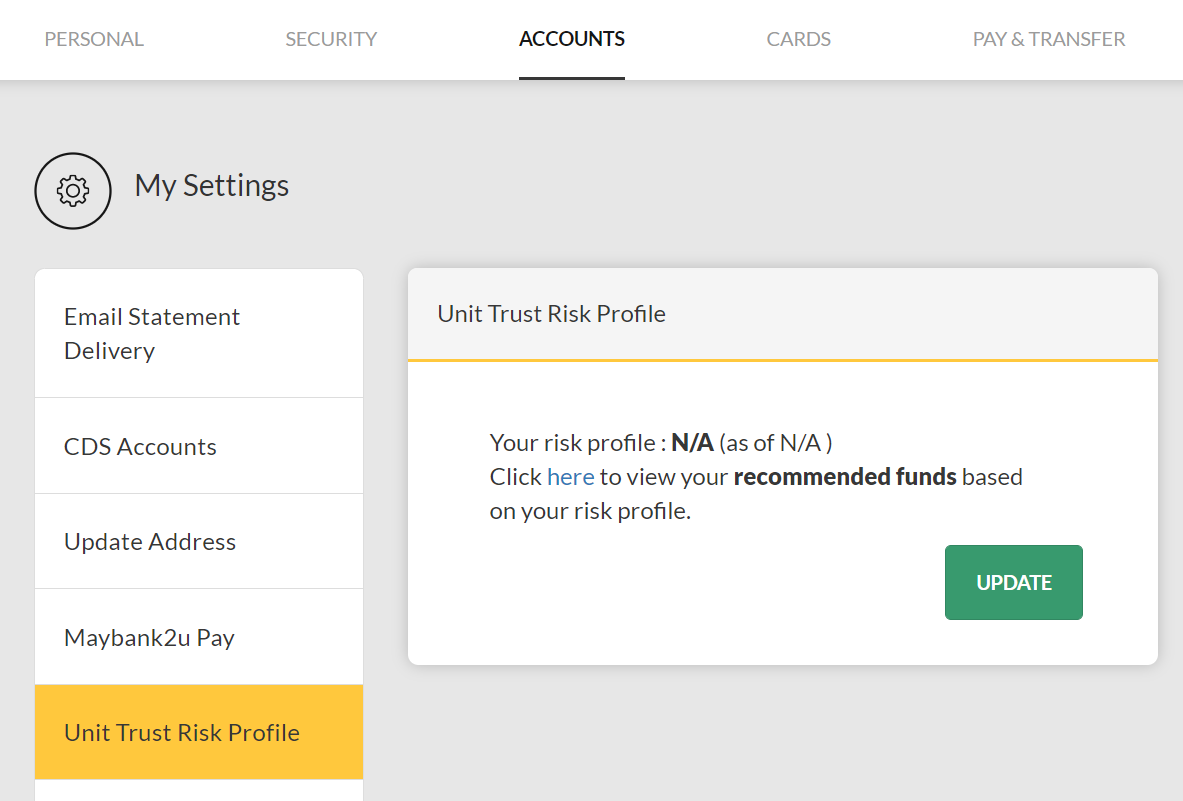

You can easily estimate your risk profile with Maybank. Just log in to your Maybank2u account, go to your profile settings, click on the ‘Accounts’ tab, then click on ‘Unit Trust Risk Profile’. Click on the ‘Update’ button to answer a short questionnaire that can help you estimate your risk profile.

Once you understand your risk profile, it becomes easier to decide how much investing risk you can take.

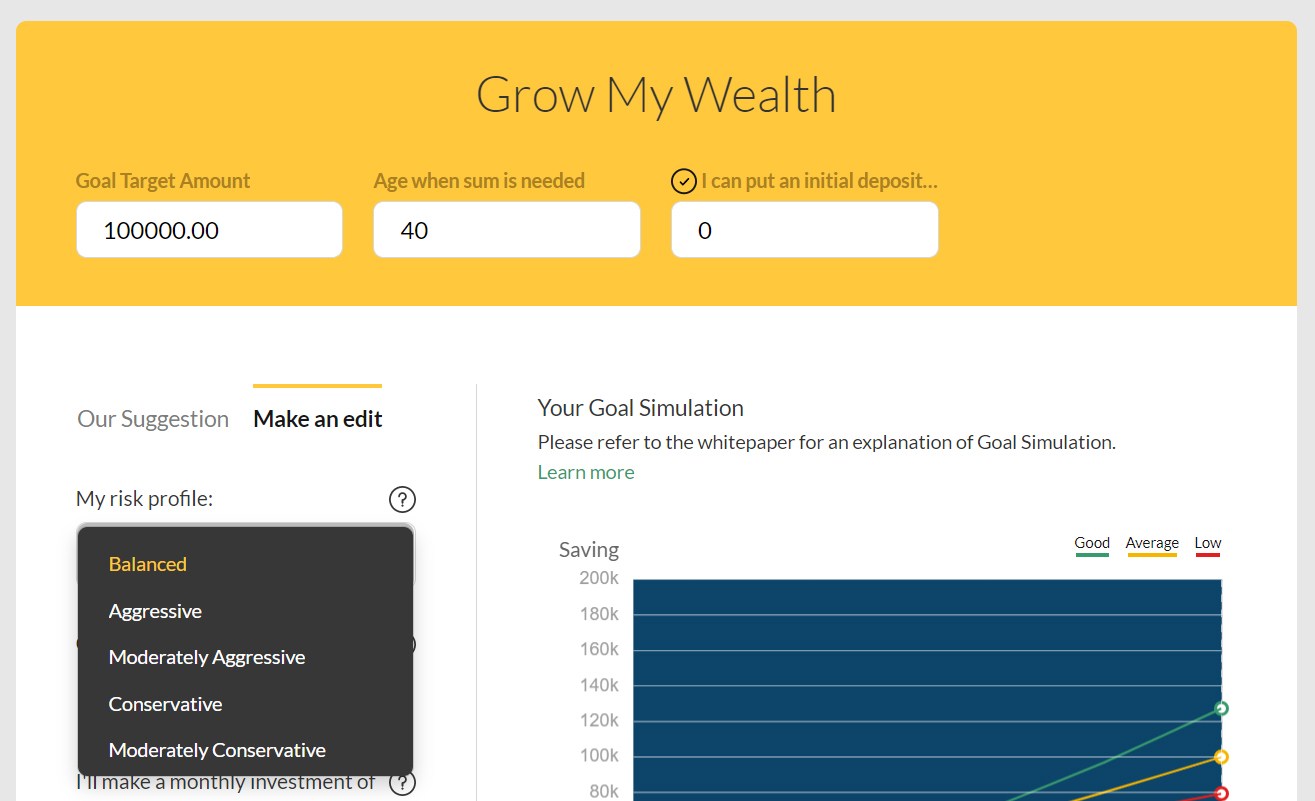

For example, you can use the Maybank Financial Goal Simulator to estimate investing outcomes. This tool can help you grow your wealth, prepare your retirement fund or save for an education fund. By default, each goal you simulate has a balanced risk level, but you can adjust this to take on more or less risk.

Depending on the risk level you choose, the Simulator will show how your portfolio can be allocated between the following four asset classes:

- Fixed Income – these consist of government securities and corporate bonds which can be local or global, issued by developed nations or emerging economies.

- Equity – these are riskier investments consisting of shares and other securities which you can buy an ownership interest, either local, regional or global.

- Cash – liquid assets like bank deposits or currency you deposit in a bank account.

- Alternatives – refer to less conventional investments like gold and REITs.

If your goal has a more conservative risk level, it may assume a higher allocation to fixed income investments. If your goal has a more aggressive risk level, it may assume a higher allocation to equities.

Knowing the risk you can tolerate is the first step to figuring out the investments that are best suited for your goals, Ultimately, this may benefit you in the long run as you invest in a way that is more in line with your risk appetite.