Imagine this: after years of education pursuing a degree, you graduate from university only to find out that just earning enough to pay off your student loan is harder than you thought and having enough spare cash to lead a comfortable life will take a lot more time and effort to achieve.

It's true that most entry-level jobs come with limited financial rewards but it's never too early to take control of your finances.

While income plays a vital role in personal finance, success will rely on how you’re managing your money. It’s cliché, but it’s true and it’s the one aspect that you can take control of. If you want to prepare yourself for a greater financial future, you must first develop a good grasp of money management. Your income alone cannot do it for you.

The good news is, you don’t have to do it by yourself, and we have all the right resources to make that feat easier for you.

List your income and spending

There’s no better way to track your money than to list down your income and your expenses. It involves identifying every bit of money that comes into your account and every sen you spend each month.

It can be quite uncomfortable for some because it involves a lot of self-confrontation: Which of your expenses are essentials? Which are just made out of a whim? Which expenses can you do without?

As simple as it may seem, it’s going to open your eyes to how you’re managing your money, and you may not be as careful with money as you think you are. It can reveal your spending issues if there’s any and ultimately help you find out where your money is going.

Itemising your expenditure for the entire month can be painstaking, but it’s a step that you cannot skip, and it’s the first step you need to take to learn to manage your money. It can be a lot of work doing it manually, but with the help of a budgeting app, it can get less taxing.

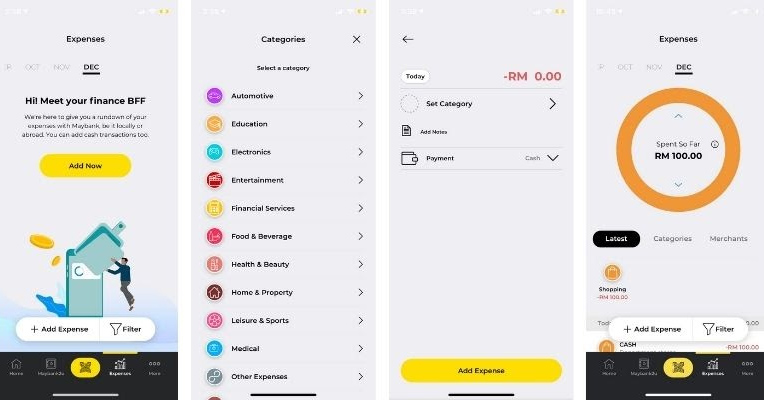

An easy way to start tracking your expenses is by using the Maybank MAE app.

It can track your expenses, automate your payments, and categorise your spending, making it easier to identify your spending habits.

This helps simplify the process and makes it easier for you to form a habit so that tracking your money can quickly become second nature!

Plan for your debt

For many Malaysians, applying for a National Higher Education Fund Corporation (PTPTN) loan may have been part of their commitments to afford a university degree. Although PTPTN loans approved after December 2008 have a low interest rate of 1% per annum, this amount will add up if you take 10, 20 or more years to repay your loan.

For example, if you have taken a loan of RM40,000 to pay for your university fees, here's how the repayment may look like:

|

Loan amount |

RM40,000 |

|

Flat interest rate per year |

1% |

|

Repayment period |

15 years |

|

Total interest amount |

RM40,000 x 1% x 15 years = RM6,000 |

|

Total monthly repayment amount |

(RM40,000 + RM6,000)/ 180 months (15 years) = RM255.56 |

Note: the example above assumes that the PTPTN loan follows the principles of Ujrah (annual flat-rate charge of 1% based on loan principal), which is applicable for all PTPTN loans approved after December 2008. If your loan was approved before December 2008, it may still be based on conventional interest charges (3% and 5% annually on your reducing balance).

So if you have happily discovered that you have RM600 left after paying your living expenses and decide to take on a new debt like buying a motorbike, remember to add your existing debt commitments first. In this case, it means adding another RM256 to your monthly commitments on top of your rental, daily commute, food and other living expenses.

The same goes for getting a new credit card. If you charge up a RM1,000 debt thinking you just need a month or two to pay it off without planning for your existing debt commitments, you could soon find yourself with more debt than you can pay off and end up owing a hefty sum of interest.

Create a budget

Tracking your expenses and identifying what needs to go and what needs to cut down is the easiest part of financial planning. The real challenge is in budgeting.

This means not just to figure out how much you need to pay for your day-to-day expenses but eventually to pay off debt and still save towards other important goals, like setting up an emergency fund, putting money aside to invest and growing your wealth.

It isn’t easy, but to avoid getting overwhelmed, take it one step at a time.

- Track your finances to find out if you are overspending and on which category? After you’ve carefully analysed how you’re spending, find out which monthly recurring expenses you can let go or reduce in order to achieve your goals.

- Follow the basic 50/30/20 rule. Try and divide your take-home pay into three spending categories: 50% for your need, 30% for your wants, 20% for your savings. You may not succeed at first but even if you manage to just save 5% of your income, that's better than nothing.

- Decide if you’re able to get to your financial goals faster by finding extra side income sources or making drastic cuts in your spending once you know where your money is going every month.

The best method to optimise your budget is by creating one! Every sen counts when you’re just starting out in your career. Once you get comfortable with the idea of sticking to a budget and managing debt in a responsible manner, you can set your sights on bigger financial goals.

Plan your financial goals

Whether you want a new gaming console, planning to afford your first car or even just pay down your debts - everyone has their own financial goals. But no matter where you are financially, the perfect time to start planning for the future is now.

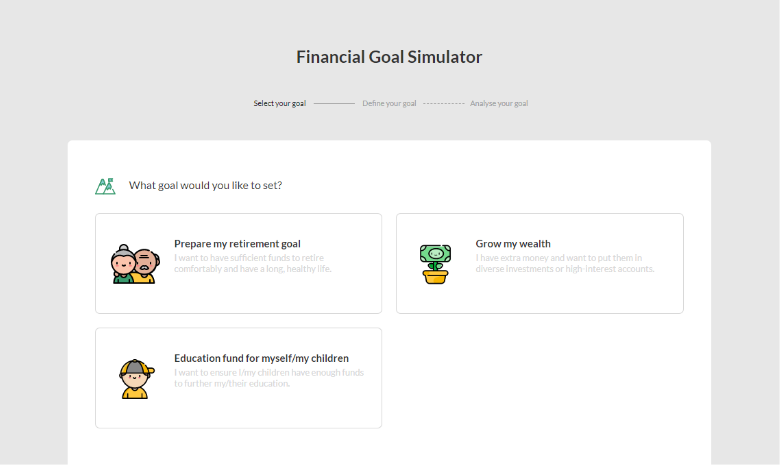

With the Maybank Financial Goal Simulator, you can create actionable steps to get started right away.

You can tackle big life goals, such as your retirement, wealth management, or education fund for yourself or your children (if you already have one). It’s easy to use and will generate a detailed plan for you instantly.

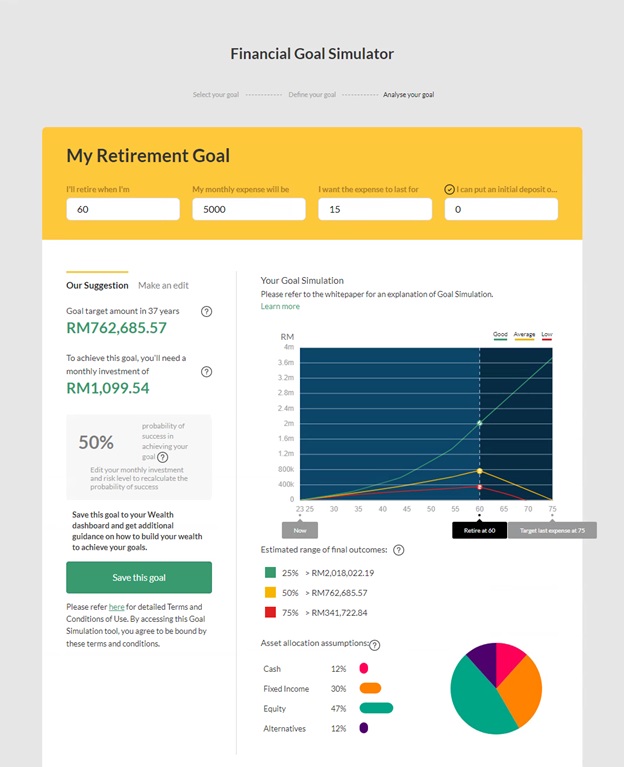

For example, if you choose “Grow my wealth”, you can set your target amount, decide how many years you want to achieve it, and how much initial investment you can put in (though not necessary).

The tool will then show you a summary of your goal, and estimate how much money you need to set aside monthly to achieve your goal.

As a new graduate, you have time as your advantage.

For example, if you set sights on saving your first RM100,000, you can use the ‘Grow My Wealth’ feature to show you the way. If you find yourself unable to afford to save more than a quarter of your income each month, you can still plan to take more time to reach your goal. The important thing is you can see your money will grow over time.

Now that you have simulated a plan, all you have to do to get started is to hit “Save this goal” and start saving!

Since you’ve officially entered adulthood, it’s the time to take your financial game to the next level. With the Maybank Financial Goal Simulator, you can learn to take charge of your life and plan your finances your way!