Need to stash your cash somewhere safe? You can access a range of deposit accounts through your bank - this includes savings accounts, current accounts and fixed deposits.

These accounts have two main similarities. First, they offer a space for you to safely deposit your money and earn a little interest. Second, they are protected by Perbadanan Insurans Deposit Malaysia (PIDM), which protects your deposits of up to RM250,000 in the event that something happens to the bank.

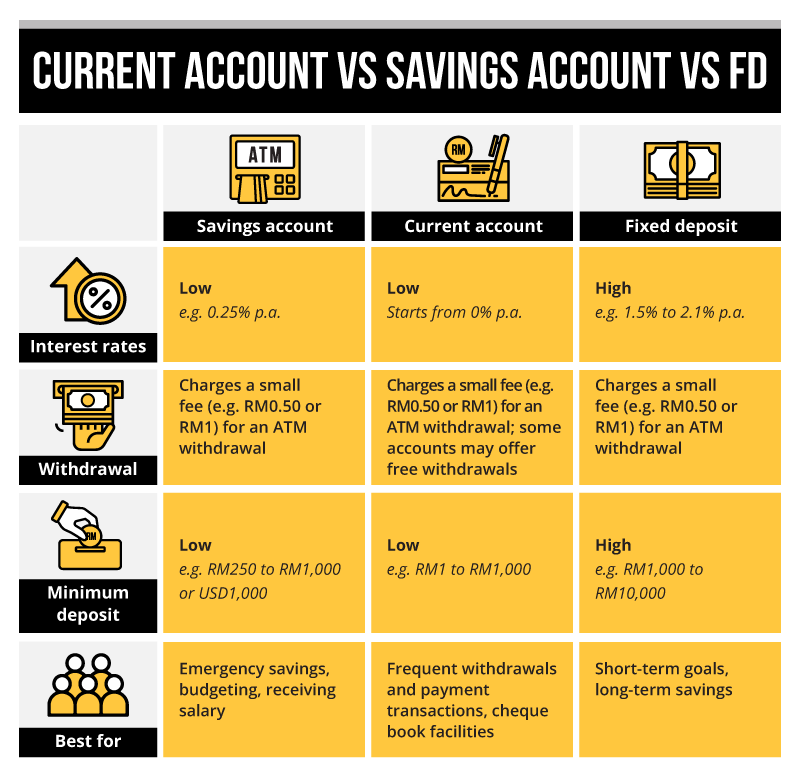

But the best account (or accounts) for you depends on what features you need. Here’s a snapshot of how savings accounts, current accounts and fixed deposits differ:

References: savings account rates; current account rates; fixed deposit rates

When do you need to use each of them?

Savings account

This is a bank account specifically designated for saving money and giving you access to those savings when you need it. In most cases, this is used as a general-purpose account. You can open an online savings account here.

With a savings account, you can:

- Use a debit card to make cashless payments

- Track current balance with a monthly bank statement

- Withdraw money from ATMs

- Set up a joint account

- Make bill payments

The tradeoff for a savings account is that it does not really do anything much for your savings. The annual interest rates are extremely low (usually less than 1% per annum). They are meant as a place to store your money and not grow it.

Current account

In many aspects, a current account (called a checking account in some countries) is the same as a savings account. Both are places to keep money if you need to access it quickly, they both have access to a debit card if you need one, and they have low minimum deposit amounts.

For most Malaysians, a savings account is enough to meet their daily and monthly needs. But if you need to issue payments with cheques, or if you make frequent transactions in and out of your account, consider a current account. You can open one online here.

With a current account, you can:

- Potentially make unlimited transactions each month with no fee, depending on account

- Track current balance with a monthly bank statement

- Use a debit card to make cashless payments

- Keep access to funds fluid to pay suppliers or transfer money to other companies

- Enjoy reduced costs on foreign fund transfers when you hold a foreign currency account

- Issue payments using cheques

- Set up a joint account

- Make bill payments

The tradeoff for this is that current accounts offer low interest returns – some accounts do not offer interest at all. The idea is that money in this account is not for saving, it’s a place where funds are stored with convenient access for constant withdrawals, transfers and payments.

Fixed deposit

While savings and current accounts are places to keep money you want to use anytime, a fixed deposit account is a place to keep it aside for a period of time. You can still withdraw the funds whenever you want to, but if you withdraw before your tenure is up, you may forfeit some interest returns.

A fixed deposit is often thought of as a low-risk investment instead of a savings tool. While this is not strictly true, it does provide better returns than keeping your money in a savings or current account for the long-term. You can open a fixed deposit online here.

With a fixed deposit, you can

- Save money while earning a higher interest

- Keep your money out of reach to avoid impulse spending

- Plan for specific goals in the coming months or years

While a fixed deposit offers higher interest returns than savings or current accounts, it does require a higher minimum deposit.

If you have money in savings and current accounts or in a fixed deposit, this is great - it probably means that you have started saving for your financial goals. However, you can do more with your idle money besides saving or keeping it locked away.

Saving is not investing

Having savings is a good thing, but it only goes so far in getting you to your financial goals. Instead, you should be thinking of making your money work harder for you.

Investing your money helps you grow your wealth, and may get you towards your goals faster. However, it may not be as easy to get started especially if you have no experience. After all, you may not even know how much you need to invest or figure out how much risk you can take on.

Fortunately for you, the Maybank Financial Goal Simulator can help. It provides resources to visualise what kind of investments you may need to achieve your dreams and gives you a clear idea of what you have to do to get there.

|

Use the Maybank Financial Goal Simulator to take the first steps towards your financial goals. |